Immigration, the bank of mom & dad, investors, low interest rates, and low supply are all driving this market.

Many people always ask me “what’s driving this Oakville real estate market?”, “how can these prices be rising so fast?”.

There are a number of reasons, not just one easy answer. Immigration numbers are a huge factor compared to the number of new housing stock being added. The greatest wealth transfer in Canadian history is another reason why people are able to afford higher prices. Low interest rates are always a factor when real estate prices soar as investors jump in to the market in large numbers. There is also a very large percentage of move up buyers that are keeping their original home in order to rent it out (if their lender allows them).

Our past and present governments have failed in planning where our immigrants are going to live and there is no quick fix to repair the damage done.

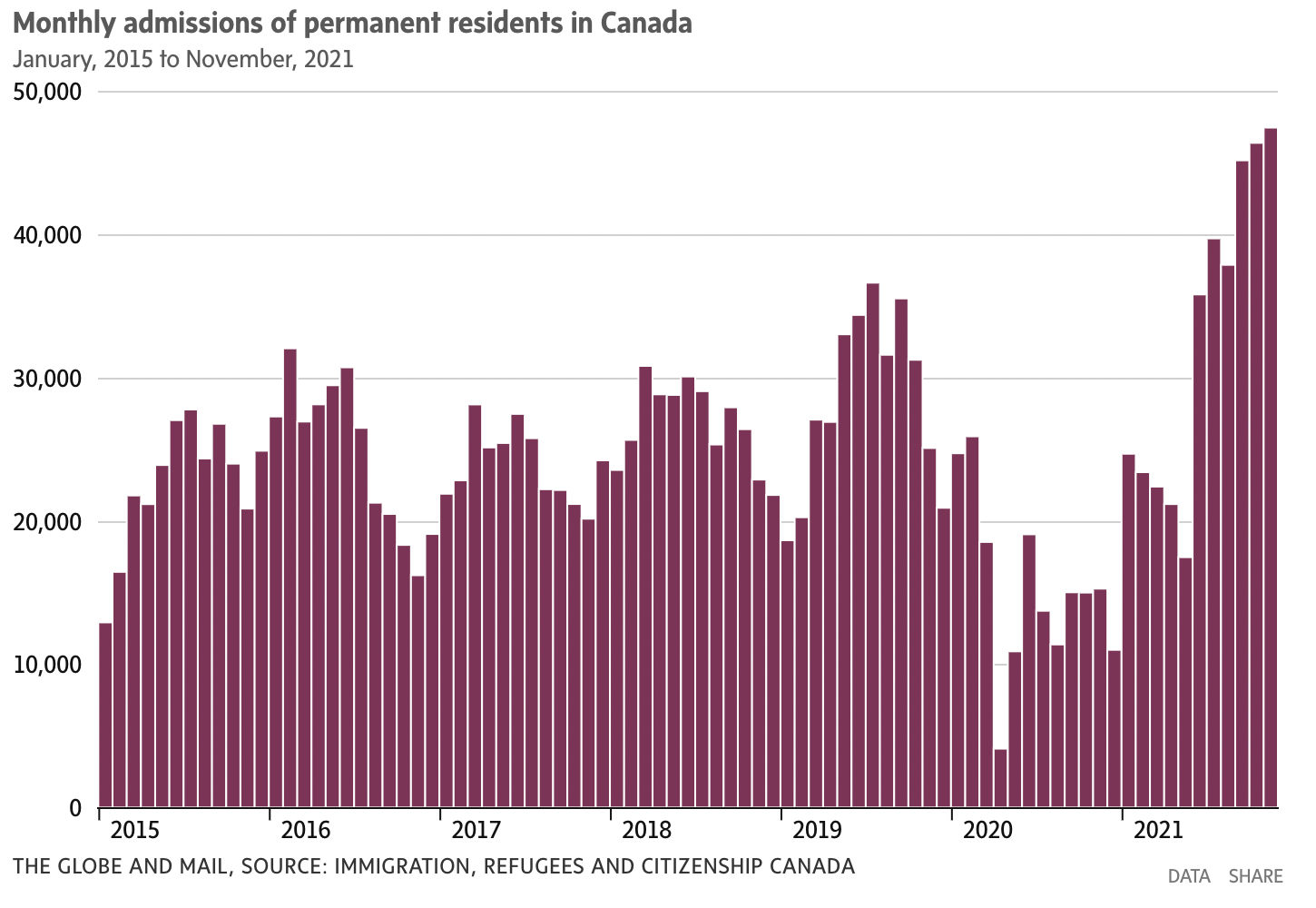

Here are the real numbers that are quite concerning:

Housing starts in the Greater Toronto Area (GTA) in 2016 was 39,027 compared to 81,480 Permanent Resident (PR) cards granted.

Housing starts in the GTA in 2017 was 38,738 compared to 86,580 PR cards granted.

Housing starts in the GTA in 2018 was 41,107 compared to 106,460 PR cards granted.

Housing starts in the GTA in 2019 was 30,587 compared to 117,770 PR cards granted.

Housing starts in the GTA in 2020 was 38,587 compared to 61,050 PR cards granted.

Housing starts in the GTA in 2021 was 41,898 compared to 141,875 PR cards granted.

There have been almost 600,000 Permanent Resident cards granted since 2016 compared to 230,000 housing units started during the same time.

Here are a number of excerpts from The Globe and Mail which support my position that our real estate prices will continue to rise despite interest rate hikes:

Feb 2022 Average Sales Prices and Sales Volume:

Freehold Townhouses

Average Price Feb 2022: $1,427,275

Average Price Jan 2022: $1,443,170

Average Price Feb 2021: $1,134,557

M.O.M. Decrease of $15,895 or -1%

Y.O.Y Increase of $292,718 or 26%

Detached Homes

Average Price Feb 2022: $2,372,754

Average Price Jan 2022: $2,498,268

Average Price Feb 2021: $1,802,469

M.O.M. Decrease of $125,514 or -5%

Y.O.Y. Increase of $570285 or 32%

Condo Apartments

Average Price Feb 2022: $818,306

Average Price Jan 2022: $839,321

Average Price Feb 2021: $613,817

M.O.M. Decrease of $21,015 or -3%

Y.O.Y. Increase of $204,489 or 33%

Condo Townhouses

Average Price Feb 2022: $1,036,432

Average Price Jan 2022: $1,079,381

Average Price Feb 2021: $797,614

M.O.M. Decrease of $42,949 or -4%

Y.O.Y. Increase of $238,818 or 30%

SHOULD I WAIT TO BUY, INCASE THE PRICES DROP?

This is another question I get every year for the last ten years, so let’s explore that scenario quickly;

1) Buy a $2,500,000 house today at a 3% interest rate with 20% down =$9500/month

2)Buy a $2,250,000 house 12 months from now at a 4.25% interest rate with 20% down =$9700/month.

*** The likelihood of prices dropping 10% over the next 12 months is incredibly low.***

My advice remains the same as it has been over the last 10 years; the sooner you buy, the less you will pay.

I’m always available for a chat about real estate. Feel free to reach out by phone any time 905-399-4269.

Categories

- All Blogs 103

- bank of Canada 36

- Bronte Oakville Real Estate 33

- Burlington Real Estate Market 2

- Fear vs Opportunity 3

- Home prices in Burlington 27

- Home prices in Milton 27

- Home Prices in Oakville 38

- interest rate 33

- Milton Real Estate Market 2

- mortgage renewal 29

- Oakville Real Estate Agent 15

- Oakville Real Estate Market Trends 12

- Real Estate Market Update Oakville Burlington Milton 20

Recent Posts